Hey there! If you’re feeling overwhelmed by your student loan payments, refinancing might be the solution you’re looking for. With so many options out there, it can be hard to know where to start. But don’t worry, we’ve got you covered. In this article, we’ll explore some of the best places to consider when refinancing your student loans, so you can make a smart choice that fits your financial goals. Let’s dive in!

Understanding the Basics of Student Loan Refinancing

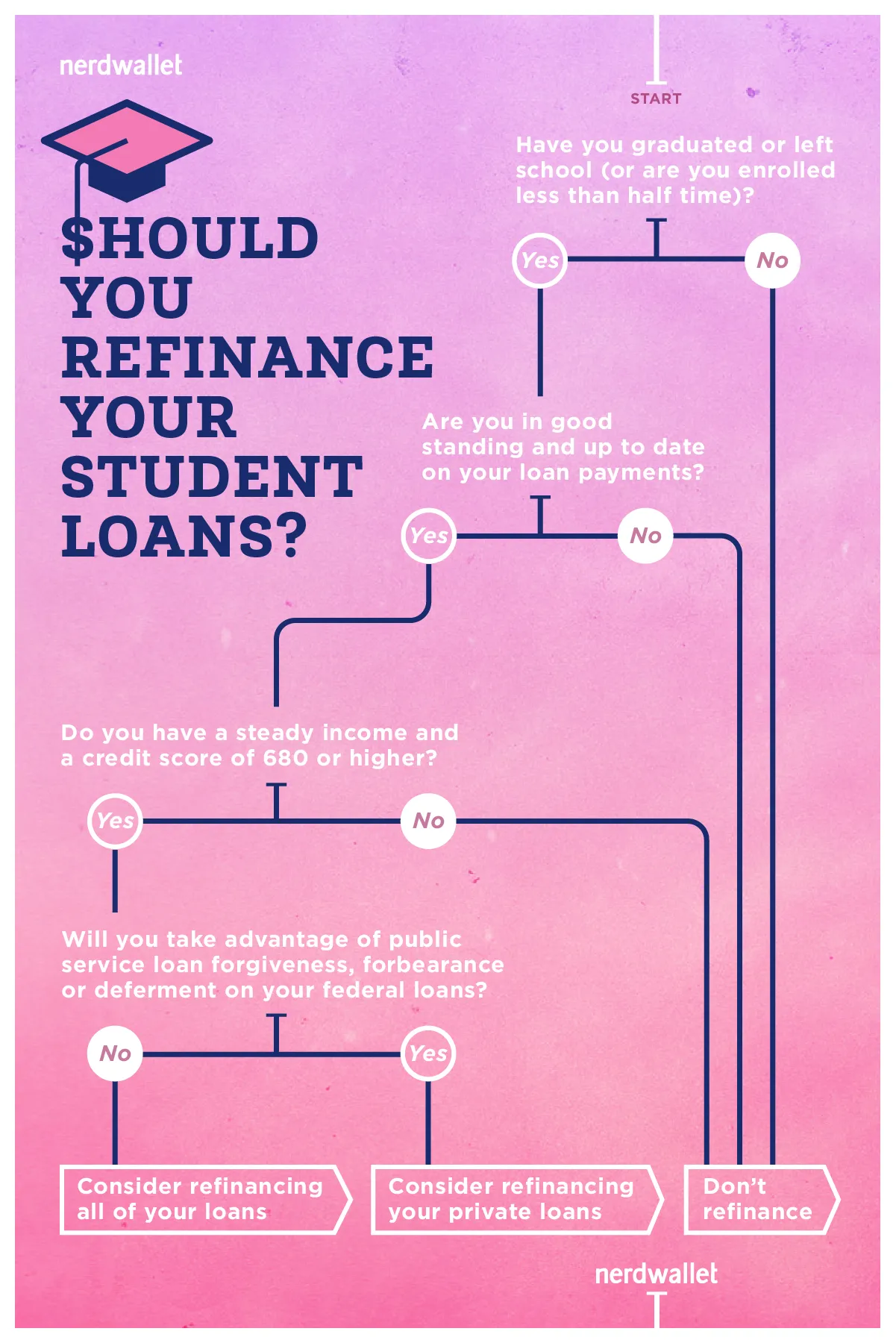

Student loan refinancing is a process where you take out a new loan to pay off your existing student loans. The goal of refinancing is to secure a new loan with better terms, such as a lower interest rate or lower monthly payments, ultimately saving you money in the long run. This can be especially beneficial if you have high-interest loans or multiple loans with varying rates.

When you refinance your student loans, you essentially combine them into one new loan with a new lender. This can help simplify your repayment process by having just one monthly payment to make instead of multiple payments to different lenders. Additionally, refinancing can potentially lower your interest rate, saving you money over the life of the loan.

It’s important to note that not everyone is eligible for student loan refinancing. Lenders typically look at factors such as your credit score, income, and debt-to-income ratio when determining your eligibility. If you have a good credit score and stable income, you are more likely to qualify for refinancing and potentially receive better terms on your new loan.

Before deciding to refinance your student loans, it’s important to carefully consider the terms of the new loan. While refinancing can save you money in the long run, it’s crucial to make sure that the new loan offers better terms than your current loans. You’ll want to compare interest rates, repayment terms, and any fees associated with the new loan to ensure that it’s the right choice for you.

It’s also worth noting that refinancing federal student loans with a private lender can result in the loss of certain federal benefits, such as income-driven repayment plans and loan forgiveness programs. If you rely on these benefits, you may want to think twice before refinancing your federal loans.

Overall, student loan refinancing can be a useful tool for saving money and simplifying your repayment process. By understanding the basics of how refinancing works and carefully evaluating the terms of the new loan, you can make an informed decision that benefits your financial future.

Factors to Consider Before Refinancing Your Student Loans

Before deciding to refinance your student loans, there are several important factors to consider. Refinancing can be a great option for some borrowers, but it may not be the best choice for everyone. Here are some key factors to keep in mind before making a decision:

1. Interest Rates: One of the most important factors to consider when refinancing your student loans is the interest rate. If you can secure a lower interest rate through refinancing, you may be able to save a significant amount of money over the life of your loan. However, it’s important to carefully compare the interest rates offered by different lenders and consider how they will impact your monthly payments and overall loan costs.

2. Loan Term: Another factor to consider when refinancing your student loans is the length of the loan term. Refinancing can allow you to extend or shorten the repayment period, depending on your financial goals. Extending the loan term can lower your monthly payments, but it may also result in paying more interest over time. On the other hand, a shorter loan term can help you pay off your debt faster, but it may also increase your monthly payments.

3. Loan Repayment Options: Before refinancing your student loans, it’s important to consider the repayment options offered by different lenders. Some lenders may offer flexible repayment plans, such as income-driven repayment or deferment options, which can help you manage your loan payments based on your financial situation. Make sure to compare the repayment options available from different lenders and choose the one that best fits your needs.

4. Fees and Penalties: When refinancing your student loans, it’s important to consider any fees or penalties that may be associated with the new loan. Some lenders may charge origination fees, prepayment penalties, or other fees that can add to the cost of refinancing. Make sure to carefully review the terms and conditions of the refinanced loan to understand any potential fees or penalties that may apply.

5. Credit Score: Your credit score plays a key role in determining the interest rate and terms you may qualify for when refinancing your student loans. A higher credit score can help you secure a lower interest rate and better loan terms, while a lower credit score may result in higher interest rates and less favorable terms. Before refinancing, take steps to improve your credit score if needed, such as checking your credit report for errors and making on-time payments on your existing debts.

By carefully considering these factors before refinancing your student loans, you can make an informed decision that aligns with your financial goals and needs. Refinancing can be a valuable tool for reducing your loan costs and managing your debt, but it’s important to weigh the pros and cons and choose the option that best fits your individual circumstances.

Comparing Different Lenders for Student Loan Refinancing

When it comes to refinancing your student loans, it’s important to shop around and compare different lenders to find the best option for your financial situation. Each lender will offer different interest rates, terms, and benefits, so doing your research and making a well-informed decision is crucial. Here are some key factors to consider when comparing different lenders for student loan refinancing:

1. Interest Rates: One of the most important factors to consider when refinancing your student loans is the interest rate being offered by each lender. Lower interest rates can save you money in the long run, so be sure to compare rates from multiple lenders to find the best deal. Keep in mind that your credit score will often impact the interest rate you are offered, so it’s important to have a good credit score before applying for refinancing.

2. Terms and Repayment Options: Another important factor to consider is the terms and repayment options offered by each lender. Some lenders may offer flexible repayment options, such as graduated repayment plans or income-based repayment plans, which can make it easier to manage your monthly payments. Additionally, some lenders may offer longer or shorter loan terms, so be sure to choose a term that works best for your financial goals.

3. Customer Service and Support: When comparing different lenders for student loan refinancing, it’s also important to consider the level of customer service and support offered by each lender. Dealing with your student loans can be stressful at times, so having access to helpful customer service representatives can make a big difference. Look for lenders that offer multiple ways to contact customer service, such as phone, email, or live chat, and consider reading reviews from other borrowers to get an idea of the level of support offered.

4. Fees and Penalties: Before choosing a lender for student loan refinancing, be sure to carefully review any fees or penalties that may apply. Some lenders may charge origination fees, prepayment penalties, or late fees, which can add to the overall cost of your loan. Be sure to factor these fees into your decision-making process and choose a lender that offers transparent pricing and minimal fees.

5. Additional Benefits: Finally, consider any additional benefits or perks offered by each lender when comparing your options. Some lenders may offer benefits such as unemployment protection, cosigner release options, or interest rate discounts for setting up automatic payments. These additional benefits can add value to your loan and make it a more attractive option.

By carefully comparing different lenders for student loan refinancing and considering these key factors, you can make an informed decision that will save you money and help you better manage your student loan debt. Remember to take your time, do your research, and choose a lender that meets your specific financial needs and goals.

How to Apply for Student Loan Refinancing

Student loan refinancing can be a great option for borrowers looking to lower their interest rates and monthly payments. Here is a step-by-step guide on how to apply for student loan refinancing:

1. Research Lenders: Start by researching different lenders that offer student loan refinancing. Look for lenders that offer competitive interest rates and flexible repayment options. You can use online comparison tools to help you compare different lenders and find the best option for your financial situation.

2. Check Eligibility Requirements: Before applying for student loan refinancing, make sure you meet the eligibility requirements of the lender. This may include having a certain credit score, income level, and debt-to-income ratio. Some lenders may also require that you have a cosigner if you do not meet all of their eligibility criteria.

3. Gather Documentation: When applying for student loan refinancing, you will need to provide documentation to the lender to verify your identity, income, and student loan information. This may include pay stubs, tax returns, student loan statements, and identification documents. Make sure to have all of these documents ready before you start the application process.

4. Complete Application: Once you have selected a lender and gathered all necessary documentation, you can start the application process. Most lenders allow you to apply for student loan refinancing online through their website. You will need to provide information about your current student loans, financial situation, and personal details. Make sure to fill out the application accurately and completely to avoid delays in the approval process.

5. Review Offer: After submitting your application, the lender will review your information and provide you with a loan offer. This offer will include details about the new interest rate, loan term, and monthly payment amount. Take the time to carefully review the offer and make sure you understand all the terms and conditions before accepting it.

6. Sign Agreement: If you decide to accept the loan offer, you will need to sign a loan agreement with the lender. This agreement will outline the terms of the new loan, including the interest rate, repayment schedule, and any fees associated with the loan. Make sure to read the agreement carefully and ask any questions you may have before signing it.

7. Pay Off Existing Loans: Once the loan agreement is signed, the lender will pay off your existing student loans on your behalf. Your new loan will then be in effect, and you will make monthly payments to the new lender according to the terms of the agreement. Make sure to set up automatic payments or reminders to ensure that you make all payments on time and avoid any late fees.

By following these steps, you can easily apply for student loan refinancing and take advantage of lower interest rates and monthly payments. Make sure to compare different lenders and carefully review the terms of the loan offer before making a decision. Refinancing your student loans can help you save money and pay off your debt faster.

Tips for Successfully Refinancing Your Student Loans

Refinancing your student loans can be a great way to lower your interest rate, reduce your monthly payments, and simplify your finances. However, before you start the refinancing process, there are a few tips you should keep in mind to ensure that you are successful in your efforts. Here are some key tips for successfully refinancing your student loans:

1. Improve Your Credit Score: Lenders will typically look at your credit score when determining whether to approve you for a loan and what interest rate to offer you. To increase your chances of getting approved for the best rates, focus on improving your credit score before applying for refinancing. Paying your bills on time, reducing your credit card balances, and monitoring your credit report for errors are all ways to boost your credit score.

2. Compare Multiple Lenders: Don’t settle for the first lender that offers you a refinancing option. Take the time to shop around and compare rates, terms, and benefits from multiple lenders. By comparing offers from different lenders, you can ensure that you are getting the best deal possible and can potentially save thousands of dollars over the life of your loan.

3. Consider a Co-Signer: If you have a limited credit history or a low credit score, you may benefit from having a co-signer on your refinanced loan. A co-signer with a strong credit history can help you qualify for better rates and terms, making it easier to refinance your student loans successfully. Just make sure that your co-signer understands the responsibilities involved and is willing to take on the risk.

4. Choose the Right Repayment Term: When refinancing your student loans, you will have the option to choose a new repayment term. Shorter loan terms typically come with lower interest rates but higher monthly payments, while longer loan terms may have higher interest rates but lower monthly payments. Consider your financial goals and budget when choosing a repayment term that works best for you.

5. Stay Organized: Once you have successfully refinanced your student loans, it’s important to stay organized and on top of your payments. Set up automatic payments or reminders to ensure that you never miss a due date. Keep track of your loan details, including interest rates, repayment terms, and lender contact information. By staying organized, you can avoid missing payments, late fees, and potential damage to your credit score.

By following these tips, you can increase your chances of successfully refinancing your student loans and achieving financial freedom. With the right approach and careful planning, you can take control of your student loan debt and save money in the process.